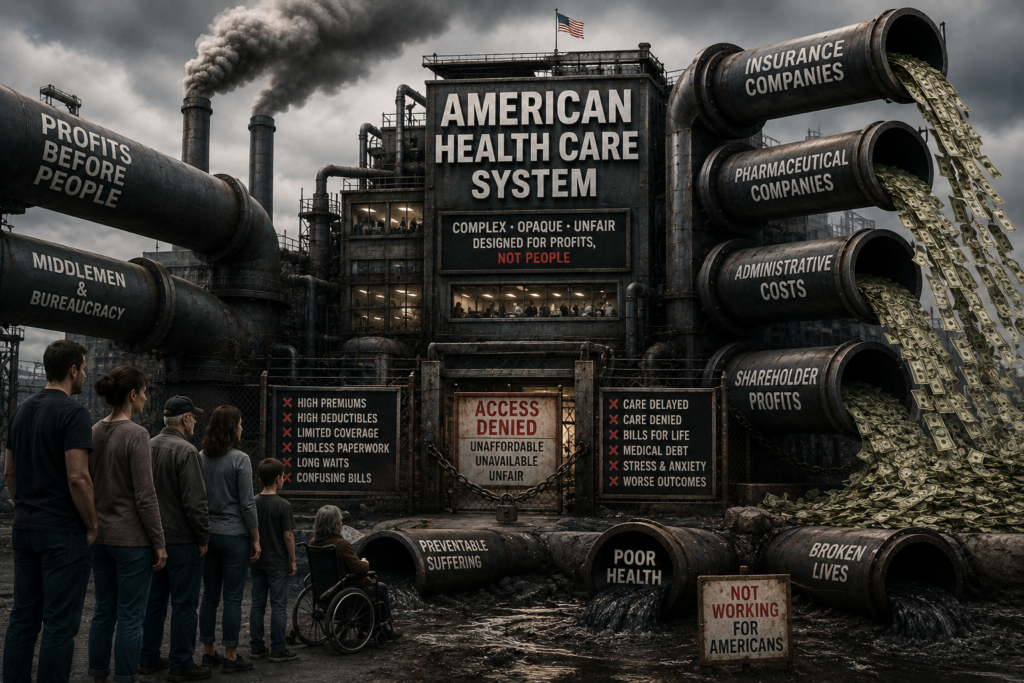

What the numbers show, what ordinary families run into, and how the insurance game actually works

Ask most Americans whether their healthcare system is working, and the answer usually depends on whether they’ve had to use it lately. Looking at the numbers instead, the answer is clearer: the United States spends far more on healthcare than any other wealthy nation yet consistently ranks last in overall performance among peer countries, spending $14,885 per person compared to the other advanced nations’ average of $5,967. Healthcare now consumes 17.2% of the entire U.S. economy, compared to 9.3% across other developed countries — roughly one of every six dollars generated in the country. Despite that spending, the United States has a lower life expectancy than its peers, and the gap has widened since the COVID-19 pandemic. The Commonwealth Fund’s comparison of ten wealthy nations found the U.S. ranked dead last in access to care, health outcomes, and overall performance, and it remains the only wealthy nation studied without a form of universal health coverage.

That’s the macro picture. The lived experience underneath it is where the real story is.

What common folks actually run into

Getting a claim denied is now routine, not rare. One in five working-age adults with private insurance reported that their insurance denied coverage for a service their own doctor recommended in the past year. Nearly 70% of people who experienced a denial said it cost them or their household more money, and 43% said the denial led to medical debt they’re still paying off. Private insurers reject roughly one in seven claims industry-wide, yet only about half of people who are denied even bother to appeal — many say they simply don’t understand their right to, or doubt it would change anything.

Prior authorization has become a second, invisible gatekeeper. Physicians and their staff now spend an estimated 13–14.5 hours a week just navigating prior authorization requests, and 93% of physicians surveyed say the process routinely delays patient care — not occasionally, but as a matter of course. On Medicare Advantage plans specifically, nearly every enrollee needs prior approval for at least some services, including hospital stays and chemotherapy, and denial rates on those requests jumped sharply in recent years before new 2026 federal rules attempted to rein it in.

Surprise bills hit even the insured. Almost half of insured Americans report receiving a medical bill for something they believed was already covered, and about one in five received a bill they either disagreed with or genuinely couldn’t afford. Medical billing itself is error-prone: a large share of bills contain at least one mistake.

Medical debt has become a mainstream American experience, not a fringe one. About 100 million Americans — not a typo — collectively owe roughly $220 billion in medical debt. It isn’t confined to the uninsured: 98% of older adults with unpaid medical bills actually have health insurance, which tells you plainly that having coverage is not the same as being protected. Medical debt shows up on credit reports, can cost people housing applications, and is linked to measurably worse mental health outcomes for the people carrying it.

The sticker price itself is often fiction, an American Healthcare Trickery— and almost nobody realizes it until they’re holding a bill. Every hospital maintains a “chargemaster,” an internal master list of prices for every service it provides, from an aspirin to an MRI. Hospitals have complete discretion in setting these numbers, and research shows chargemaster prices commonly run more than four times the actual cost of delivering the care. Almost nobody actually pays that price. A Johns Hopkins analysis of over 2,300 hospitals found that cash prices and commercial insurers’ negotiated rates both land, on average, at roughly 58–64% of the chargemaster figure — meaning the “list price” functions less like a real price and more like an opening bid in a negotiation the patient never gets to sit in on. One hospital’s own billing FAQ offers a plain example: a listed charge of $4,000 for a service, with the insurer’s actual negotiated rate at $1,000 — a fourfold gap for the same care.

Here’s where it gets genuinely disorienting: even the “negotiated” insurance rate isn’t necessarily a fair one. RAND Corporation research has found private health plans pay hospitals an average of roughly 224% of what Medicare pays for the same services — and because coinsurance is typically calculated as a percentage of that negotiated rate (commonly 10–20%), an inflated negotiated rate directly inflates what the insured patient owes out of pocket. Insurers, meanwhile, have limited incentive to fight hard for lower rates: many are legally required to spend 80–85% of premium revenue on patient care, meaning a bigger overall “pie” of healthcare spending can mean bigger absolute dollars for the insurer even as the percentage stays fixed — and any losses in a bad year can simply be recovered through higher premiums the next.

For patients without insurance, the exposure is often worse. Since 2021, federal rules have required hospitals to post a “discounted cash price” for self-pay patients, but that price is still commonly 2–5 times what Medicare pays for the same service — and the default bill that arrives in the mail is frequently the full, undiscounted chargemaster rate unless the patient knows to proactively ask for the cash-pay discount. Few people know that question even exists to ask. And if care happens to come from an out-of-network provider — sometimes without the patient’s knowledge, such as an anesthesiologist at an in-network hospital — the hospital can “balance bill” the patient for the gap between the chargemaster price and whatever the insurer was willing to allow, a practice federal “No Surprises Act” protections have curbed but not eliminated.

The practical upshot is almost the opposite of how the system is supposed to work: a cash-paying patient willing to simply ask for the self-pay or discounted rate sometimes ends up owing less than an insured patient would after deductibles and coinsurance are applied to an inflated negotiated rate. That single fact is disorienting the first time you encounter it, because it inverts the basic assumption most people carry into the system — that having insurance is what protects you from being overcharged. It’s central to understanding why the system feels so opaque from the patient’s side: the “sticker price” was never meant to be paid by anyone, but it quietly determines what almost everyone actually pays. Moreover, hospitals and insurers make it genuinely difficult to get the cash price for a service, often steering patients back toward billing through insurance by default.

I had a minor issue and needed an MRI. My insurance covers it after the deductible. It was approved, and I was told that my share is $250 of the $1950 total. The in-network provider does not show a price list; when asked, they claim not to know and point to a never-ending phone loop. I used Claude and Google to search. Learned that if I go to a different provider, my cost could be in the range of $350- $500. So, my insurance company is eating my premium money every month, and $100 -$250 when I need the service.

What they should do is list the services they offer with the price point. Even if it is a full price. Patients need to know what it will cost for a service.

Similarly for prescriptions, I can find better prices than insurance by going with GoodRx or CostPlus or similar other providers. I may not need to pay a monthly premium.

Most people, when they need the service, are not mentally there to shop for the best price or have the time to do so. The current American healthcare system takes advantage of Americans when they are most vulnerable and most in need of help.

The insurance conversation worth having

Given all that, it’s worth stepping back and asking a more basic question: what is health insurance actually for? The honest answer, and the one increasingly echoed by healthcare economists, is that insurance works best as protection against low-probability, high-cost events — not as a prepaid card for routine care. When it’s used as the latter, the overhead of premiums, deductibles, prior authorization, and network restrictions can end up costing more than it saves for people with low routine utilization.

That reframing opens up a few strategies more people are exploring, particularly younger, healthier adults:

- A high-deductible health plan paired with a Health Savings Account. The HSA carries a genuine triple tax advantage — pre-tax contributions, tax-free growth, and tax-free withdrawals for medical expenses — with 2026 contribution limits of $4,300 for individuals and $8,550 for families. Unspent funds roll over indefinitely and, after age 65, can be withdrawn for any purpose, functioning much like a second IRA. For someone in good health, the strategy is to let the HSA compound untouched while paying small routine expenses in cash.

- Direct Primary Care combined with a catastrophic plan. A growing number of physicians have opted out of insurance billing entirely, charging a flat monthly membership (roughly $50–$100) for unlimited visits and same-day access, paired with a lower-cost catastrophic policy that only kicks in for genuine emergencies.

- Cash-pay for routine prescriptions and labs. Services like GoodRx, Cost Plus Drugs, and direct-to-consumer lab pricing frequently beat what a person would pay through insurance once premiums and cost-sharing are factored in — a detail many people never discover simply because “check if insurance covers it” is the automatic first move.

None of this is a case for going without coverage. The catastrophic piece is the non-negotiable part of the strategy — one serious accident, one cancer diagnosis, one cardiac event changes the math completely, and that’s exactly the scenario real insurance exists to protect against. The point isn’t to avoid insurance; it’s to stop mistaking it for something it was never designed to be, and to recognize that the industry’s profitability depends in part on most people never running these numbers themselves.

For those on Medicare, the picture shifts but the same logic applies. Part A is free for most people; Part B becomes progressively more expensive if you delay enrollment past 65; and for Medicare Advantage enrollees, the annual task of comparing Part D drug plan costs against actual cash-pay pricing through GoodRx or similar services is often worth the twenty minutes it takes — insurance-negotiated drug pricing doesn’t automatically beat the cash price, especially for common generics.

What other countries do differently

Every other wealthy peer nation — through single-payer systems like the UK and Canada, regulated multi-payer models like Germany and Switzerland, or hybrid approaches like France — guarantees coverage to nearly everyone and caps how far a family’s finances can be wiped out by illness. None of them ask ordinary patients to become amateur billing experts just to avoid financial ruin. That doesn’t mean those systems are free of tradeoffs — longer waits for non-urgent elective care are a real and often-cited cost of single-payer systems. But it does mean the burden of navigating the system doesn’t fall so heavily on the sickest and least-resourced people, which is precisely where the American system currently places it.

The bottom line

America’s healthcare system has genuine strengths — specialized and acute care, rapid access to specialists once you’re in the door, and research that leads the world. But for the person filing a claim, fighting a denial, or opening a bill they didn’t expect, those strengths are cold comfort. A system that spends twice what its peers do and still leaves 100 million people holding medical debt isn’t failing because Americans don’t work hard enough to navigate it — plenty of them navigate it brilliantly, the way any of us learn to navigate a maze we’re forced into. It’s failing because the maze shouldn’t be there in the first place.

We did not get here overnight. And we will not get out of it overnight. The insurance, the Pharma, the hospital network systems have no incentive to change. Americans need to prioritize and demand change in the American healthcare system.